TOOLS AND CALCULATORS

Tools and calculators can make the decision-making process easier by helping you figure out where you stand now—and where you'd like to end up in the future—so you can invest more wisely today.

STAY INFORMED

Read up on the latest from Voya experts to help you retire better. VIEW BLOG

If a participant is eligible to a distribution of Roth assets (contributions and earnings), the distribution is considered qualified if:

- A period of five years has passed in which the first contribution (including rollovers) was made to the Roth account; and

- the participant has experienced one of these events:

- Attainment of age 59½

- Disability

- Death

If the requirements for a qualified distribution are not met, and the assets are not rolled-over to another eligible plan, the earnings portion of the distribution will be taxable.

To illustrate how contributing toward retirement affects your paycheck, let’s assume you earn $40,000 in taxable income annually and you want to defer $50 from each paycheck to the deferred compensation plan. You’re paid every other week or 26 times a year.

| Without savings | With 457 plan | With Roth | |

| Salary per pay period | $1,538 | $1,538 | $1,538 |

| 457 savings contribution | $0 | $50 | $0 |

| Taxable salary | $1,538 | $1,488 | $1,538 |

| Taxes at 20% | $307 | $297 | $307 |

| Roth savings contribution | $0 | $0 | $50 |

| Take home pay | $1,231 | $1,191 | $1,181 |

| Difference in take home pay | $0.00 | $40.00 | $50.00 |

This hypothetical example assumes a filing status of single with no dependents, no deductions or exemptions. This chart assumes a hypothetical effective tax rate of 20% on taxable salary. This example is not guaranteed and your actual results may vary. Systematic investing does not ensure a profit nor guarantee against a loss in declining markets. You should consider your financial ability to consistently invest in up as well as down markets.

For a relatively small ($40 or $50) difference in your take home pay, you can start building a retirement resource to help you meet your future retirement objectives!

Click here for time sensitive info about your plan.

If you find retirement planning puzzling, you’ve come to the right place. This is where you can find information as well as try out some online tools and start putting the pieces of your retirement plan together!

Think of your retirement as a puzzle with four large pieces:

- Social Security

- KPERS/KPF

- Johnson County 457(b) and 401(a) Plans

- Personal Saving

Normally a puzzle with just four pieces would be considered simple. It’s not quite as simple, though, when it comes to planning for retirement and meeting your retirement objectives. Determining whether you are on track to achieve your retirement goals involves assessing various factors and considering your individual circumstances. You don’t have to do it alone, though.

This site features information, resources, and tools to show you how the retirement planning pieces fit together so you can take control of your financial future.

It’s Your Retirement Plan - Piece by Piece!

Not FDIC/NCUA/NCUSIF Insured I Not a Deposit of a Bank/Credit Union I May Lose Value I Not Bank/Credit Union Guaranteed I Not Insured by Any Federal Government Agency

Insurance products, annuities and retirement plan funding issued by (third party administrative services may also be provided by) Voya Retirement Insurance and Annuity Company, One Orange Way, Windsor, CT 06095-4774. Securities are distributed by Voya Financial Partners LLC (member SIPC). Custodial account agreements or trust agreements are provided by Voya Institutional Trust Company. All companies are members of the Voya® family of companies. Securities may also be distributed through other broker-dealers with which Voya has selling agreements. Insurance obligations are the responsibility of each individual company. Products and services may not be available in all states. CN4147085_0127

Invest in you with the Johnson County 457(b) Plan

All eligible Johnson County employees are enrolled in the Johnson County 457(b) Deferred Compensation Plan as active, but not contributing, participants. You must agree to defer a minimum of $10 or 1% per pay period to contribute to the 457(b) Plan, but you can change or stop contributions at any time.

When you save, Johnson County saves for you too. The county will match up to 4% of your base bi-weekly salary in the Johnson County 401(a) Defined Contribution Plan when you contribute to the Johnson County 457(b) Plan. Log into your account now to change your savings rate.

You can change your savings rate online at any time, but use the Johnson County Participation Agreement Form if you’d rather make the change by form. This will allow you to make changes to your pre-tax, Roth after-tax, and catchup deferral options. Return the completed form to:

Johnson County, Kansas

Financial Management and Administration

111 S. Cherry, Suite 2400

Olathe, KS 66061-3486

Fax: 913-715-0577

Investments in Target Retirement Funds are subject to the risks of their underlying funds. The year in the fund name refers to the approximate year (the target date) when an investor in the fund would retire and leave the workforce. The fund will gradually shift its emphasis from more aggressive investments to more conservative ones based on its target date. An investment in the Target Retirement Fund is not guaranteed at any time, including on or after the target date.

Vanguard, Admiral, Windsor, and the ship logo are registered trademarks of The Vanguard Group, Inc.

Please visit joco.timetap.com or contact the local Voya office in Overland Park at (913) 661-3797 to schedule an appointment to review and discuss your retirement planning strategy.

Investment adviser representative and registered representative of, and securities and investment advisory services offered through, Voya Financial Advisors, Inc. (member SIPC).

Plan overview

Johnson County sponsors a 457(b) Deferred Compensation Plan and a 401(a) Defined Contribution Plan for employees. To learn more about the features and benefits of participating in the Johnson County Retirement Plans, visit joco.voya.com.

Plan Highlights

Eligibility

All county employees who have attained age 18 and who fall within the following classifications are eligible:

- Regular full-time employees scheduled for 80 hours or greater per pay period;

- Part-time benefits eligible employees who are in position of .50 full-time equivalent or greater; and

- Elected officials and appointees of the county.

Independent contractors and leased employees are not eligible.

457(b) Contributions

Participants contribute through a reduction in salary, referred to as a "deferral." You must elect to defer a minimum of $10 or 1% per pay period. The maximum annual contribution amount is as follows:

| YEAR | ANNUAL MAXIMUM |

| 2026 | $24,500 for Ages 49 and under $32,500 for Ages 50-59 or 64+ (Additional $8,000 over the Ages 49 and under limit) $35,750 for Ages 60-63 (Additional $11,250 over the Ages 49 and under limit) $49,000 under the 457 special election catch-up (Additional $24,500 over the Ages 49 and under limit) |

Higher annual limits are available for participants who have attained age 50 during the calendar year. The 457 special election catch-up may be available for participants in the three years prior to the year of their designated normal retirement age based on the amounts they could have contributed in previous years but did not. Contact the local Voya office in Overland Park at (913) 661-3797 for assistance with determining your contribution limit for the year. For more information on contribution limits, visit voya.com/irslimits.

Please note, you may not use both the Age 50+ catch-up and the 457 special election catch-up provision during the same calendar year. You must select the provision which provides the higher contribution amount.

401(a) Contributions

All contributions under the Johnson County 401(a) Plan are made by the county. You are eligible to receive a county matching contribution if you defer a minimum of $10 or 1% per pay period to the 457(b) Plan. The matching contribution is discretionary and may change from year to year. It is based on the amount you contribute to the 457(b) Plan.

Employee contributions to the Johnson County 401(a) Plan are not permitted.

401(a) Vesting

Upon severance from employment, you will be vested in (have earned ownership of) all or a portion of your 401(a) account balance based on the applicable vesting schedule below:

The vesting schedule, based on your number of years of service with the county, is as follows:

| For Elected Officials of the county: | |

| 1 year | 25% |

| 2 years | 50% |

| 3 years | 75% |

| 4 years | 100% |

| For all other employees: | |

| 1 year | 20% |

| 2 years | 40% |

| 3 years | 60% |

| 4 years | 80% |

| 5 years | 100% |

Notwithstanding the above schedules, you would be 100% vested in your Johnson County 401(a) Plan account upon your attainment of normal retirement age (age 65), your death, your total and permanent disability, the discontinuance of employer contributions to the Plan, and the termination of the Plan.

Roth Contributions

You have the choice to make contributions to the Johnson County 457(b) Plan on a pre-tax basis, a Roth after-tax basis, or a combination of both sources. To compare your options to determine which is right for you, please review the Johnson County 457(b) Roth overview brochure.

Voya Retirement Advisors, LLC, powered by Morningstar Investment Management LLC

To help you feel more in control of your financial future, Johnson County has teamed up with the investment professionals at Voya Retirement Advisors, LLC (VRA) to offer advice and guidance personalized for 457(b) Plan participants.

VRA's advisory services let you choose from two simple solutions based on your level of investment experience and the amount of time you want to spend managing your retirement plan account.

Prefer a helping hand while still maintaining control over your investments? Then consider the Online Advice option that provides investment advice and educational tools at no additional cost to you.

Want investment professionals to manage your account for you? With the Professional Management fee-based program you not only get personalized advice and guidance from the investment professionals at VRA but also have a service that puts those recommendations into action for you.

For more information, visit joco.voya.com to log into your account. Click Get Investment Advice and follow the prompts to choose the option that works for you.

IMPORTANT: Projections or other information generated by VRA regarding the likelihood of various retirement income and/or investment outcomes are hypothetical in nature, do not reflect actual results (including investment results) and are not guarantees of future results. Results may vary with each use and over time.

Advisory Services provided by Voya Retirement Advisors, LLC (VRA). VRA is a member of the Voya Financial (Voya) family of companies. For more information, please read the Voya Retirement Advisors Disclosure Statement, Advisory Services Agreement, and Advisory Services Overview. You may also request these from a VRA Investment Advisor Representative by calling your plan's information line. VRA has retained Morningstar Investment Management LLC as an independent “financial expert” (as defined in the Department of Labor’s Advisory Opinion 2001-09A) to develop, design, and implement the asset allocations and investment recommendations generated by the Advisory Services. Morningstar Investment Management LLC is a federally registered investment adviser and wholly owned subsidiary of Morningstar, Inc. Neither VRA nor Morningstar Investment Management LLC provides tax or legal advice. If you need tax advice, consult your accountant or if you need legal advice consult your lawyer. Future results are not guaranteed by VRA, Morningstar Investment Management LLC or any other party and past performance is no guarantee of future results. The Morningstar name and logo are registered trademarks of Morningstar, Inc. All other marks are the exclusive property of their respective owners. Morningstar Investment Management LLC and Morningstar, Inc. are not members of the Voya family of companies.

Loans

Loans are not available under the plan(s).

Contact local service team

Local service support from experienced representatives is available to all Johnson County employees.

Overland Park office

11101 Switzer Rd, Suite 130

Schedule an appointment

joco.timetap.com

Telephone

(913) 661-3797

Office hours

8:00 a.m. to 4:00 p.m. CT

You can also contact your local representatives directly.

Marisa Brown

Phone: (913) 661-3759

Email: Marisa.Brown@voyafa.com

Bill Hirschler

Phone: (913) 661-3771

Email: William.Hirschler@voyafa.com

Julie Kurland

Phone: (913) 661-3763

Email: JKurland@voyafa.com

Investment adviser representative and registered representative of, and securities and investment advisory services offered through, Voya Financial Advisors, Inc. (member SIPC).

Toll-free Customer Service

Voya’s national toll-free telephone line, (800) 584-6001, provides Johnson County 457(b) Plan participants with customer service support weekdays from 7:00 a.m. - 8:00 p.m. CT (excluding stock market holidays).

Internet Access

Access your account online here or through the My Account link at the top of the page. In your Johnson County Retirement Plans account online, you can:

- Monitor your balance and investments.

- Make investment election changes.

- Update your contributions to the 457(b) Plan.

- Update your personal and contact information.

- Estimate your progress towards your retirement goals.

- Access investment option information and performance.

The 4-1-1 on 457(b) Plans

One of the main pieces of the retirement planning puzzle is an employer-sponsored retirement plan. Most government and some non-government employers in the United States offer a 457(b) Deferred Compensation Plan.

There are two types of contributions that can be made to the Johnson County 457(b) Plan. You can save for retirement on a pre-tax basis (also known as a Traditional 457), a Roth after-tax basis, or a combination of both sources.

Here are the basic differences between the two:

Pre-tax

- No taxes on contributions now

- Withdrawals taxed as ordinary income later

- Contributions reduce your adjusted gross income

- Earnings are tax-deferred until withdrawn

- Rollovers are allowed to other qualified plans and IRAs

- Required minimum distributions start at the later of age 73 (if born before 1960; age 75 if born in 1960 or after) or retirement

Roth after-tax

- Pay taxes on contributions now

- Withdrawals are tax-free later

- Contributions are subject to income tax withholding

- Earnings are tax-deferred until withdrawn

- Withdrawals are federal tax-free (qualifying conditions apply)

- Rollovers are allowed to another Roth 457(b) or Roth IRA

- No required minimum distributions

Whether you contribute on a pre-tax basis, Roth after-tax basis, or a combination of both:

- You decide, within IRS limits, how much of your income you want to defer.

- Johnson County will reduce your paycheck by that amount.

- You decide how your contributions are invested, utilizing one or more investment options available in the Johnson County Retirement Plans.

- Your 457(b) contributions have no effect on the benefits you will receive from Social Security. Your Social Security contributions and benefits (if applicable) will be based on your total pay, including the amounts paid into the 457(b) Plan.

- Pre-tax amounts in the 457(b) Plan are subject to the required minimum distribution (RMD) rules. A participant must begin taking annual distributions from the account by the later of age 73 (if born before 1960; age 75 if born in 1960 or after) or retirement. An IRS 25% penalty tax applies to any RMD amount not taken in a timely manner.

Which is right for you?

Once you’ve made the decision to contribute to the Johnson County 457(b) Plan, you need to look at how much and which contribution source is right for you.

Consider pre-tax contributions if you…

- Want to enjoy the benefits of deferring taxes

- Need to take home as much pay as possible

- Expect to be in a lower tax bracket in retirement

Consider Roth after-tax contributions if you…

- Like the idea of tax-free income in retirement

- Expect your salary to increase over time

- Can afford a reduction in take-home pay

Consider both pre-tax and Roth after-tax contributions if you…

- Aren’t sure whether your taxes will be lower or higher when you retire

- Want to diversify your tax strategy

- Still want to reduce your current taxable income

You should always seek the advice of a tax attorney or tax advisor prior to making a tax-related insurance/investment decision. The Voya® family of companies does not offer legal or tax advice.

The Johnson County Retirement Plans

The Johnson County Retirement Plans are a 457(b) Deferred Compensation Plan and 401(a) Defined Contribution Plan. All Johnson County employees are automatically pre-enrolled in the 457(b) Plan to help make it easier to plan for their financial future today. Features of the Johnson County Retirement Plans include:

- Matching Contributions: Johnson County will match up to 4% of your base bi-weekly pay and invest it into the Johnson County 401(a) Plan.

- Investment Variety: The 457(b) and 401(a) Plans offer an array of investment options for you to choose from. The investment options available in each Plan are designed to help achieve different investment objectives. You can transfer your assets and future contributions among the investment options in the Plans to help reduce investment risk, subject to Voya’s Excessive Trading Policy.

- Advice and Guidance: Johnson County has teamed up with the investment professionals at Voya Retirement Advisors, LLC (VRA) to offer advice and guidance personalized for participants. VRA's advisory services let you choose from two simple solutions, Online Advice at no additional cost and the fee-based Professional Management, based on your level of investment experience and the amount of time you want to spend managing your accounts.

- Catch-up Contributions: Higher annual limits are available for participants who have attained age 50 during the calendar year. The 457 special election catch-up may be available for participants in the three years prior to the year of their designated normal retirement age based on the amounts they could have contributed in previous years but did not. Contact the local Voya office in Overland Park at (913) 661-3797 for assistance with determining your contribution limit for the year.

Have a COLA!

The IRS limits how much a participant can contribute annually to their employer-sponsored retirement savings plan. The limits are subject to change each year. The change is known as a Cost of Living Adjustment (COLA). Your local Voya representatives for Johnson County can help determine what your contribution limit is this year based on your age and years until retirement. For additional information, visit voya.com/irslimits.

Not FDIC/NCUA/NCUSIF Insured I Not a Deposit of a Bank/Credit Union I May Lose Value I Not Bank/Credit Union Guaranteed I Not Insured by Any Federal Government Agency

Insurance products, annuities and retirement plan funding issued by (third party administrative services may also be provided by) Voya Retirement Insurance and Annuity Company, One Orange Way, Windsor, CT 06095-4774.

Securities are distributed by Voya Financial Partners LLC (member SIPC). Custodial account agreements or trust agreements are provided by Voya Institutional Trust Company. All companies are members of the Voya® family of companies. Securities may also be distributed through other broker-dealers with which Voya has selling agreements. Insurance obligations are the responsibility of each individual company. Products and services may not be available in all states.

The Kansas Public Employees Retirement System (KPERS) is a defined benefit retirement plan that provides a pension benefit for life. Even though you may be only beginning your career, it’s important to start planning for your future today. Your KPERS pension is just one piece in the puzzle that is retirement planning.

KPERS includes three statewide retirement plans for state and local public employees:

- The Kansas Public Employees Retirement System

- The Kansas Police and Firemen's Retirement System (KP&F) and

- The Kansas Retirement System for Judges

Kansas law requires that all eligible employees employed by a KPERS employer are automatically enrolled and immediately become members. As an active member, you contribute a percentage of your gross earnings and your contributions earn interest annually. You automatically earn service credit for the years you work in a covered position. After a number of years of service, you are guaranteed a monthly retirement benefit for the rest of your life. This is called "vesting" your benefit.

KPERS has struggled with a long-term funding shortfall for more than a decade. Members are living longer and retiring earlier, which can increase liabilities. For over 18 years, state statue has kept employers from contributing at the rate required for proper funding, and the Great Recession in 2008 caused unprecedented investment losses. Changes were made in 2012 by the Kansas Legislature to answer this shortfall.

Log into your account at kpers.org to discover more about your KPERS benefit.

You can:

- Calculate your estimated KPERS retirement benefit.

- Get a personalized snapshot of how the changes may affect you.

- Learn more about your KPERS benefits.

For more information:

- Call your KPERS representative at

(888) 275-5737. - Email your KPERS representative at kpers@kpers.org.

Getting Personal (Savings)

No matter how diligent you’ve been in contributing to the Johnson County 457(b) Plan, how many service credits you’ve earned for KPERS, and how long you’ve contributed towards Social Security, your retirement planning puzzle may not be complete without income from personal savings.

Personal savings can be extremely helpful, and maybe necessary, to fill any possible income gaps in your retirement plan. Whether you are wondering how to save more in the Johnson County 457(b) Plan for retirement or are at the point in your career where you know you need to put more money aside during your remaining working years, one of the best ways to help find more money to save is by creating and managing a budget.

A budget can help you prioritize your spending, create an emergency fund for unexpected expenses, and save for personal financial goals. A budget can also help you determine how much you can afford to save for tomorrow while meeting the financial demands of today.

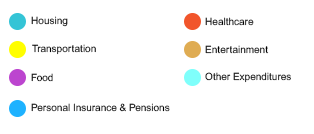

Where does my money go?

According to the 2023 U.S. Bureau of Labor Statistics consumer expenditures report, the breakdown of essential expenses for the average American looks like this:

According to the consumer expenditures report, the average income before taxes in 2023 was $101,805. The average annual expenditures were $77,280, or 75.9% of the average income before taxes. How close are the Bureau of Labor’s percentages to your own? To answer that question, you’d have to sit down and work out a budget.

Think about the things you spend money on each month. If you just stay on top of your bills without a larger understanding of monthly income and your spending habits, it’s difficult to get a sense as to how much money you have to work with.

Where to start?

- Collect your last three months of bills. Categorize where your money goes each month and see if there's a pattern. Is your spending predictable or is it inconsistent?

- If it’s inconsistent, look at six months instead of three. This will help you get a better sense of where your money goes. Once you have an idea of the things you need to spend money on and the things you want but don’t necessarily need, you can start to think about spending and saving for the long-term.

- When making a big purchase such as a new home or car, remember to consider how it would impact your spending and saving plan.

Find the balance between your needs, wants, and savings

Visit voya.com/tool/budget-calculator to help stay on track for retirement by creating a 50/30/20 budget that is personalized to your priorities and situation.

The 50/30/20 approach to budgeting is a simple strategy that suggests you put up to 50% of your after-tax income toward needs (things you must have or can’t live without), 30% toward wants (things you can cut back on or do without), and 20% toward savings (money for future needs such as an emergency fund, retirement, and financial freedom).

In the beginning, setting up a budget can take a little time. For the first few months, sticking to your budget may require some discipline. In time, spending and saving according to your budget can become as common as paying your bills. In the end, that work to create and stick to a budget can really be worth the effort.

Most of us have grown up with a basic understanding of Social Security. It provides monthly benefits that replace part of the earnings that are lost when a worker retires, becomes disabled, or dies. Since its inception, most people have thought of Social Security as a given and for a long time that was true.

The challenge now facing Social Security is that many people currently working in the U.S. are part of the biggest labor force ever, the Baby Boomers. As Baby Boomers become eligible for Social Security, though, it has begun paying out more than it is taking in. This may cause challenges for future recipients both in terms of how much they will receive and how much they will need to supplement their retirement income from other sources.

What’s Your Normal Retirement Age (NRA)?

NRAs can be slightly different from person to person but most can begin receiving Social Security retirement benefits as early as age 62. Enter the year of your birth in the box below to see your NRA.

Over 70 million Americans receive a Social Security benefit as of August 2025.2

The current Social Security monthly retirement benefit check averages $1,955.48 (approximately $23,466 annually), $1,575.30 for survivor benefits (approximately $18,904 annually), and $1,445.72 for disability insurance (approximately $17,349 annually). Could you live comfortably on that?

Visit ssa.gov/myaccount to create a my Social Security account that provides personalized tools for everyone, whether you receive benefits or not. You can use your account to request a replacement Social Security card, check the status of an application, estimate future benefits, or manage the benefits you already receive.

2 Social Security Administration; Research, Statistics, & Policy Analysis. Monthly Statistical Snapshot, August 2025.

Need help with your retirement planning puzzle? You don’t have to do it alone.

Voya® offers educational tools and resources to help you get and stay on track for retirement. Visit joco.voya.com to register or log into your account and get started.

Financial wellness is about the balance of living for today, saving for tomorrow, and building confidence along the way. To help guide you, log into your account and select the Financial Wellness tab at the top of the page. Complete your personal assessment to measure yourself across the six pillars of financial wellness and learn how to take meaningful actions for your financial future.

Orange Money is the money you need to save for retirement, versus green money, which can be spent now. The educational, interactive myOrangeMoney® online experience shows you how your current retirement savings may translate into monthly retirement income. It outlines where you stand today, highlights areas that need improvement, and lets you take immediate action to improve your readiness with an interactive slider.

IMPORTANT: The illustrations or other information generated by the calculators are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. This information does not serve, either directly or indirectly, as legal, financial or tax advice and you should always consult a qualified professional legal, financial and/or tax advisor when making decisions related to your individual tax situation.